A Quick Hit of Market trends

Overall, PE deals are down and are looking to stay that way

Between high interest rates, rising labor costs, and inflation woes, macro forces continue to slow PE deals. Where the buyers are pulling back, the sellers are pushing in. As cited by Bass Berry & Sims, the market remains frothy with sellers looking to offload admin burden and the pinch of the payors.

“Many commentators believe the current slump may continue through 2024—that we should be bracing for a longer than normal winter. The New York Federal Reserve did not allay these concerns when it announced last month that the U.S. is more likely than not (i.e., has a 56% chance) to fall into a recession by September 2024. The next quarter and indeed the next year, then, may continue to be highlighted by small, strategic expansions and creative cross-sector transactions.”

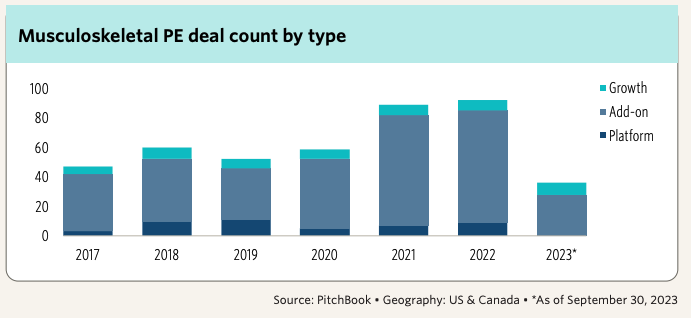

However orthopedic deals still make up a substantial portion of physician practice management deals.

.png)

ASCs continue to grow in de novo and acquisitions

Orthopedics remains the most popular specialty for ASCs, with around 2,233 ortho-centric facilities currently.

However, pain management ASCs are rapidly growing, reaching 2,162 facilities and nearing orthopedics in volume.

This growth is driven by the shift to non-opioid pain treatment.

FTC cracking down on PE-backed anesthesia group

The FTC's recent crackdown on healthcare consolidation, exemplified by its lawsuit against US Anesthesia Partners, signals a heightened scrutiny of mergers and acquisitions in the sector.

This move reflects a growing regulatory focus on maintaining competitive markets and could have significant implications for future healthcare consolidation strategies.

The Biden administration has sought out several antitrust cases mostly with little traction. It will be worth watching how the USAP case will unfold, especially when their financial sponsor is Welsh Carson, the sponsor behind United Musculoskeletal Partners (UMP).

Additional thoughts

PE is a leading indicator, which is why I follow it closely. Whether it be PE, a large health system, or fellow orthopedic groups joining together, size and scale provide leverage. With the macro forces working against independent practices, payors are taking notice and will use this as an opportunity.

Finding ways to compete more effectively in the market and generate new revenue streams outside of the payor-sphere will be critical. Whether that need is 12 months or 12 years remains dependent on the market you operate in.

Links:

Q3 2023 Healthcare Services Report

Healthcare trends & transactions Q3 2023

One thing I’m thinking about:

Hinge prepares for IPO. What will we learn?

Valued at $6.2B after their latest raise and with $400M in the bank, Hinge is a digital health juggernaut.

While they’re already on our collective radar, Hinge’s move to the public market signals the public’s acceptance and hunger for tech-driven healthcare solutions to reduce the cost of care. The question is, will that be proven when they have the spotlight of public markets analyzing their data?

In the coming months, Hinge will release a trove of never-before-seen data on their operations and financials, starting with their S1 filing. This will be the first look behind any digital PT company’s curtain and I’m excited to see what we can learn.

I’m not one for predictions but I’d sure be surprised if they are north of $6.2B 12 months after IPO.

.png)

One conversation starter:

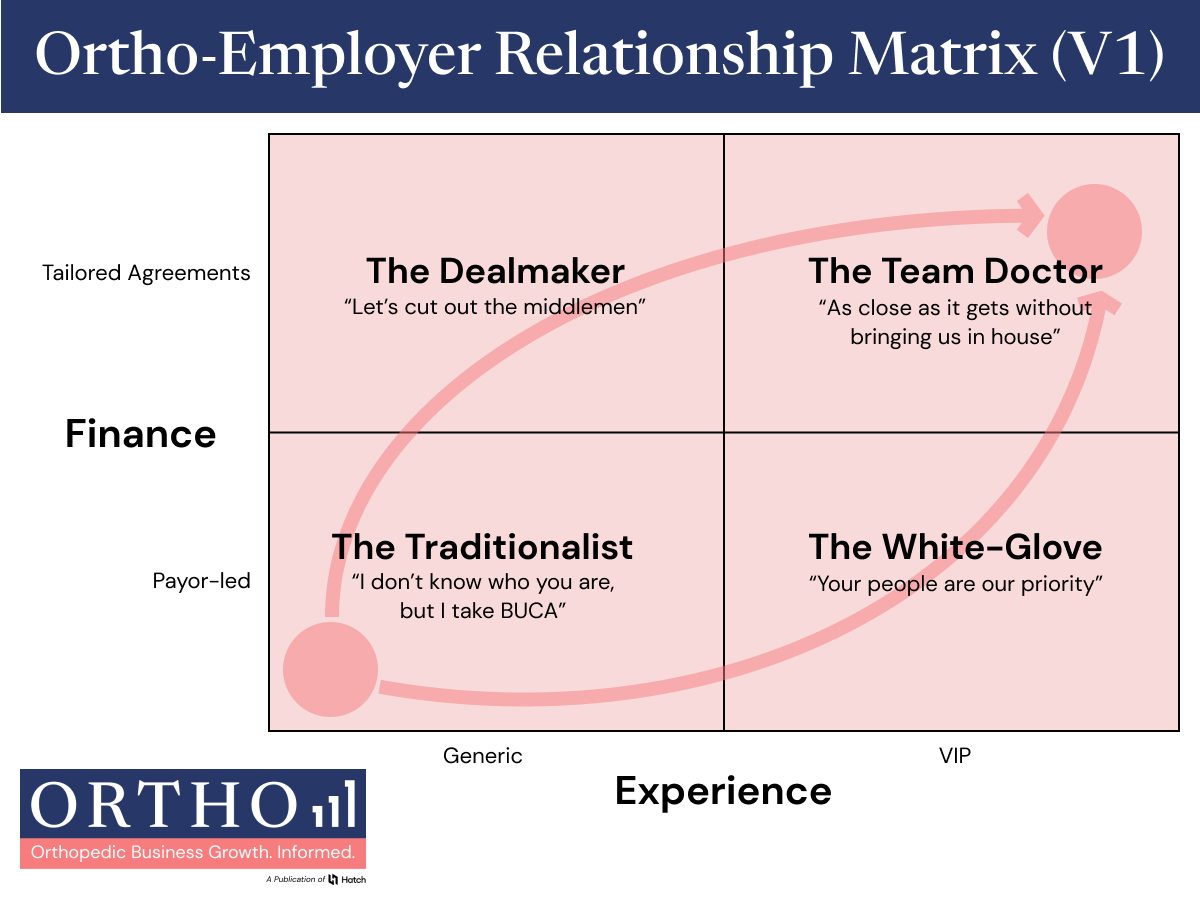

How do you think about the employer relationship spectrum?

I’ve noticed something interesting with our Ortho customers.

While each has an ultimate goal of developing a strong direct-to-employer strategy, approaches vary.

Nothing wrong with that.

MJ and Lebron are two of the greatest – but each took their own path.

However, it got me thinking about the different dimensions of the ortho-employer relationship.

We took a minute to sketch two dimensions we’re seeing on a matrix.

Some groups we work with are more interested in creating direct financial agreements with employers. Think bundled rates, eliminating copays, or direct contracting.

While others are focusing on building out a “VIP” experience and taking that to employers. Think real-time triage, video consultations and visits, or priority scheduling.

I think you need a good bit of both to create a long-term, differentiated, and defensible relationship with employers.

I also think that meeting a customer (employer) where they are is critical, so being willing to tailor your offering to meet their needs is of the utmost importance.

But what do you think?

What are the tangible attributes that define your employer relationship? And what, if anything, should come first when building the infrastructure to reach the promised land?

Copyright © 2024 Hatch.